Unnamed officials at the Guam Department of Education used $24.6 million in federal funds to buy 34,503 laptops mostly through one vendor without a fixed-term contract and without evidence of a legal procurement. Of those laptops, 1,693 of them “totaling $1.5M procured via small purchases covered by 45 purchase orders (POs), which appeared to be artificially divided.” These are according to an audit released today by the Office of Public Accountability.

The allegedly illegal procurements occurred largely during the pandemic, which pre-dates the term of the new superintendent of education, Erik Swanson. Public Auditor Benjamin Cruz noted that he ordered the audit on request from GDOE recently, though he did not specify whether Mr. Swanson or former interim superintendent Judith Won Pat made the request.

The audit also revealed that GDOE purchased twice as many laptops as there are students.

“The MUNIS record showed that 14,285 laptops already in inventory prior to the purchase of the additional laptops, were still usable at the end of FY 2022,” the audit states. “With the 34,503 purchased during FY 2021 to FY 2022, laptops available for use totaled 51,603. For GDOE Public School use, GDOE purchased 29,531 or 2,034 more laptops than its 27,497 student population (School Year 2020- 2021). If the existing laptops are to be considered in the laptop requisitions, there appears to be an excess purchase of 16,319 laptops for public school use.”

Also, the audit found the procurements occurred without the signature of the attorney general, which is required by law. Just days ago, the governor’s office issued a statement complaining that a recent decision by the attorney general that effectively halts procurement throughout most agencies – including GDOE – is impeding government operations. Attorney General Douglas Moylan, in a February 28 legal memo to 21 GovGuam agencies including the governor’s office, temporarily withdrew his office’s legal services to those agencies, which includes the signing off on procurements.

The basis of his decision is a pending question before the courts on whether the OAG can both represent GovGuam agencies and prosecute officials within them for corruption. Guam’s Rules of Professional Conduct for attorneys prohibit such a perceived conflict of interest, but Mr. Moylan is asserting that particular rule cannot apply to the OAG, which is charged by the Organic Act to perform both duties. Until the question is settled, Mr. Moylan has elected to prosecute allegedly corrupt officials over representing their agencies.

The irony is that, in the legal memo, Mr. Moylan identified the 21 agencies along with the primary precursor of the corruption investigations: 23 audit reports by the OPA alleging illegal activities on the part of several officials throughout those 21 agencies.

Chris Barnett, whose legislative committee has oversight of the GDOE, issued the following statement in reaction to the audit:

“When I met with OPA prior to audit’s release, I was told the audit contained actionable items the AG could move on. I couldn’t agree more. To read about $23M in questioned costs is a travesty when anyone can take a look around our school system and see how that money could have been used better to benefit our kids.”

Mr. Cruz sent today’s released audit to Mr. Moylan’s office. And for only the second time on record regarding the release of an audit, he made a public and written commentary:

“The Guam procurement law along with GDOE’s standard operating procedures should guide its procurement of goods and services to ensure that public resources are used wisely. Our review of GDOE’s procurement of laptops found that there was no agreement/contract executed, which significantly violated specification/requirement of a Firm Fixed Price Agreement required in the IFB. As a significant amount of federal funds was used to purchase these laptops, GDOE needs to institute corrective measures to prevent more recurrences and ensure efficient use of local and federal resources.”

Here is the audit’s executive summary in its entirety:

The Guam Department of Education (GDOE) purchased 34,503 laptops valued at $24.6 million (M) in fiscal year (FY) 2021 through FY 2022. Our review of documents relative to procurement processes, purchases and distributions, grant budget, and applicable internal controls found some indications of apparent improper purchases generally arising from the following:

a) Noncompliance with procurement laws, regulations, and GDOE internal policies and Standard Operating Procedures (SOP);

b) Questionable excessive laptop purchases and distributions; and c) Significant weaknesses in internal controls.

We questioned the cost of $23.1M for laptops purchased under the Invitation for Bid (IFB)- Indefinite Quantity Bid (IQB) No. 019-2020, which were not covered under an agreement/contract with its sole vendor, Vendor A. Section 3.2.7, Contract Type, of IFB–IQB No. 019-2020 specifically states that “A Firm Fixed Price agreement will be consummated between the most responsible bidder and GDOE.” We also questioned the cost of 1,693 laptops totaling $1.5M procured via small purchases covered by 45 purchase orders (POs), which appeared to be artificially divided.

The apparent indications of improper purchases arising from questionable excessive purchases are evidenced by deficiencies such as: a) failure to implement the required procurement processes, b) failure to execute the required documentation and approvals, c) lack of reasonable and realistic determination of need, d) distributions not based on ultimate end-user need outlined in the distribution plan, and e) others. Additionally, we found weak internal controls over the review and approval processes and the discrepancies between MUNIS records and physical counts. We also found inadequate physical controls, which are some significant factors indicative of weaknesses in internal controls over the purchasing, distribution, and management of the laptops. Although the purchases were federally funded by United States Department of Education (USDOE) grants, the non-adherence to the required procurement processes and internal control deficiencies could potentially result in waste and abuse of funds.

Evidence of Noncompliance of Procurement Rules, Regulations, Internal Policies, and SOPs

We reviewed procurement documents under IFB-IQB No. 019-2020 IQB of Technology Equipment, Supplies, and Accessories, which authorized the purchase of significant quantities of laptops during FY 2021 and FY 2022. Our review covered 26 POs (42% out of 62 POs issued) valued at $23.5M. Of the 26 POs, only 16 POs valued at $23.1M were referenced to IFB-IQB No. 019-2020 while other POs were procured via small purchase. Our review identified evidence of noncompliance with the Guam Procurement laws and regulations and GDOE internal SOP.

1. No Evidence of the Office of the Attorney General’s Involvement Throughout the Procurement Process

Pursuant to Title 5 of the Guam Code Annotated (GCA) §5150, whenever the Chief Procurement Officer conducts any solicitation or procurement which is estimated to result in an award of $500 thousand (K) or more, the Attorney General (AG) or his designees, including one or more Special Assistant Attorneys General (SAAG) who may be so designated or appointed by the AG, shall act as a legal advisor during all phases of the solicitation or procurement process. Additionally, the AG or his designee, including one or more SAAGs, shall determine the correctness of form and legality when approving contracts.

Except for AG Form No. 012 (Notification of Procurement Over $500K) signed by GDOE Procurement Officer, Form No. 014 (Declaration Re: Compliance with 5 GCA §5150) signed by the GDOE Superintendent, and Form 008 (Procurement Review Checklist for IFB) signed by the GDOE Legal Counsel, there were no other records provided to document the GDOE Legal Counsel or Office of the Attorney General of Guam’s (OAG) participation on the succeeding procurement activities consummating in the agreement/contract execution, review and signing.

2. No Agreement/Contract with Solely Awarded Vendor A

Section 3.2.6, Contract Type, of IFB-IQB No. 019-2020 states that “A Firm Fixed Price agreement will be consummated between the most responsible bidder and GDOE.” In GDOE SOP 200-026 (Competitive Sealed Bidding-IQB) and SOP 200-027 (Competitive Sealed Bidding- IFB), Step 14 states that “if the IFB is $500K and over, the buyer will submit the procurement file to legal for review and processing prior to processing a Purchase Order.” If the IFB is for construction or non-professional services, the Buyer will prepare the procurement file, provide it to the GDOE Legal Counsel and request that the GDOE Legal Counsel prepare the contract. After internal review, the procurement file is submitted to the GDOE Legal Counsel, who prepares the contract for signatures, which includes the AG and the Office of the Governor (OOG). The PO shall be issued after the contract is signed by all parties, However, the SOP does not explicitly mention procurement of “supplies.”

Despite several written requests for a copy of the agreement/contract signed by the GDOE officials and Vendor A, none was provided. We subsequently learned that no agreement/contract was ever executed. Consequently, the laptops valued at approximately $23.1M purchased under IFB-IQB No. 2019-2020 were not covered with a Firm Fixed Price Agreement, required in the IFB, thus was neither approved by the AG nor the OOG. We questioned the purchase of these laptops aggregating $23.5M, which significantly violated the IFB specification/requirement of a Firm Fixed Price Agreement.

3. IQB Review Requirement Not Performed

Under GDOE SOP#200-026 IQB Step 15 of the Step-by-Step IFB Process, every six months, the buyer must consult with the End User to determine if the IQB should remain in place. A determination letter should be drafted, which is reviewed by the Supply Management Administrator (SMA) to ensure appropriate support is provided before signing it. Furthermore, Step 16 states that IQBs can only be placed for a period of one year with the option to extend for no more than 90 days when the SMA determines in writing that it is not practical to award another contract at the time of such extension.

We found no evidence that the required every six months’ review was performed, and a determination letter was executed, signed, and filed. However, a memo (to the procurement file) was subsequently provided relative to the determination to extend the IQB Contract that was signed by the SMA on December 13, 2021, specifying the extension period effective from December 2021 until March 2022. The determination memo did not disclose the non-practicability of awarding another contract. Furthermore, there was no documented agreement between GDOE and Vendor A for such extension, since there was no initial agreement/contract executed.

4. Inaccurate Disclosure in Certification of Completed Procurement Record

Title 5 of GCA §5250 and Title 2 of the Guam Administrative Rules and Regulations (GAR), Division 4, Procurement Regulations, §3130 states that no procurement award shall be made unless the Chief Procurement Officer, the Director of Public Works, or the head of a purchasing agency certifies in writing under penalty of perjury that he has maintained the record required by §3129 of these regulations and that it is complete and available for public inspection. The certificate is itself a part of the record.

In our initial inspection of the IFB-IQB No. 019-2020 procurement file, the Certification of Completed Procurement Record was not signed by the GDOE Superintendent. Item 19 (contracts including draft versions) was marked on file. A Certification of Completed Procurement Record was subsequently provided, which was signed by the GDOE Superintendent on Nov. 18, 2020. Similarly, the signed certification showed item No. 19 (contract including draft versions) was marked as on file. However, in our follow-up review of the procurement record, no contract was seen on file. The inaccurate disclosure and incomplete procurement record maintained for the IFB- IQB No. 019-2020 exhibited a lack of transparency and accountability.

Questionable Laptop Purchases and Distributions

1. PO Quantity versus IFB Minimum Requirement

Section 2.3, Project Description–Minimum Hardware Requirements/Specifications, of IFB-IQB No. 019-2020, stated the minimum requirement for basic laptop (1,804 units), admin laptop (275 units), and Chromebook (100 units).

We found that POs referenced to this specific IFB, identified quantities ordered/purchased significantly exceeding the minimum hardware requirements stipulated in the IFB. The minimum hardware requirement for the three types of laptops totaled 2,179 units, however, laptops purchased per the 16 POs totaled 32,799, an excess of 30,720 units or 1,410%.

The 16 sampled POs for 32,799 units with a total value of $23.1M were supported with determinations of need (DONs), which generally stated the need to procure laptops/ tablets for distance learning and face-to-face instruction for social distancing. The DONs prepared from August 2020 through March 2022 do not specify the quantities needed to support the POs. We found that 13 POs were signed under the Purchasing Authority/Certifying Officer portion by the Third Party Fiduciary Agent (TPFA) Senior Grant Manager and three POs were signed by its Director.

The IFB is for an indefinite quantity of laptops and due to fluctuation of needs, the quantities may increase during the award period. However, the excessive quantities purchased compared with the minimum hardware requirement per the IFB appeared not properly analyzed and reviewed and thus needs to be justified.

2. Purchases Exceeded Public School Student Population

The MUNIS record showed that 14,285 laptops already in inventory prior to the purchase of the additional laptops, were still usable at the end of FY 2022. With the 34,503 purchased during FY 2021 to FY 2022, laptops available for use totaled 51,603. For GDOE Public School use, GDOE purchased 29,531 or 2,034 more laptops than its 27,497 student population (School Year 2020- 2021). If the existing laptops are to be considered in the laptop requisitions, there appears to be an excess purchase of 16,319 laptops for public school use.

Furthermore. GDOE purchased 4,970 laptops in addition to existing inventory of 2,817 for private schools, charter schools, and other support departments. We cannot determine the potential excess due to the unavailability of count of ultimate end users from these groups. Although these purchases using federal grants were approved by the TPFA representatives based on DONs and POs, we questioned the excess of laptops purchased over the recorded student population.

3. Unopened and Undistributed Laptops

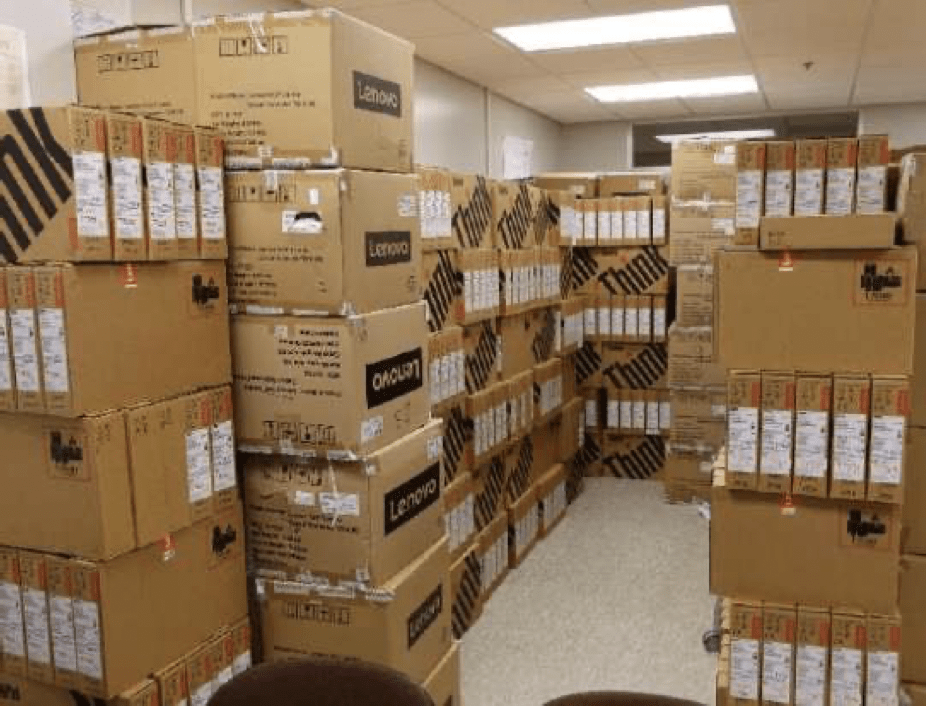

During a visit with the GDOE Internal Audit Office (IAO) in November 2022, we were shown the storage room at GDOE headquarters with an estimated 1,200 laptops still in their original boxes. These laptops are those assigned to the Curriculum and Instructional (C&I) Office. In the MUNIS inventory records, 1,497 laptops were distributed to the C&I office, with an existing inventory of 80.

Although the majority of these laptops were delivered to C&I in June 2021, these were first seen in storage on November 18, 2022, and again on February 14, 2023 (image at the right). Non-distribution of these laptops signifies that the laptops were not urgently needed, thus a questionable determination of ultimate end users need. Furthermore, during the OPA and GDOE IAO site visits to 10 schools in May 2023, we found five schools still had unused laptops in boxes. The number of laptops in their original boxes ranged from 14 to 66.

Although the majority of these laptops were delivered to C&I in June 2021, these were first seen in storage on November 18, 2022, and again on February 14, 2023 (image at the right). Non-distribution of these laptops signifies that the laptops were not urgently needed, thus a questionable determination of ultimate end users need. Furthermore, during the OPA and GDOE IAO site visits to 10 schools in May 2023, we found five schools still had unused laptops in boxes. The number of laptops in their original boxes ranged from 14 to 66.

The non-distribution of these laptops indicates a flaw in the internal control in planning requisitions and distributions. It reflects ineffectiveness in determining the need for the laptops and the timeliness of their distribution.

4. Questionable Small Purchase

5 GCA §5213- Small Purchase

Small purchase requirements shall not be artificially divided to constitute a small purchase. Our review of 10 other POs totaling $432K, which were not referenced to IFB-IQB 019-2020 but were procured via a small purchase method of solicitation, disclosed the following:

High-end Specifications and High Cost Small Purchases

In addition to the 32,799 laptops purchased valued totaling $23.1M via IFB–IQB, GDOE purchased an additional 246 laptops valued at $427K via nine POs, using the small purchase solicitation method. We noted high-end laptops with high unit costs ranging from $989 to $3,879 were purchased for student/teacher needs. POs were based on Request for Quotations (RFQ), which specify the quantity and the model/type of laptop intended to be purchased. The six vendors for these POs were either not awarded with laptops or non-bidders as they did not submit bids for the IFB. Two of these POs had items not awarded or had unit costs not in the IQB awarded listing.

Additionally, there were no summaries for bids received or bid abstracts to document the responders to the RFQ, comparison of quotations received, determination of lowest bidder awarded, and the approval of the awarded vendor. POs for these small purchases were not signed by the vendor to signify acceptance.

Appearance of Artificial Division

Title 5 of GCA §5213 specifies that a small purchase should not be artificially divided to constitute a small purchase. Of the sampled POs, nine POs for 246 units with a total value of $427K had amounts between $1,978 and $249K, thus appeared to be artificially divided so as not to exceed the federal threshold of $250K for small purchases. Furthermore, 36 POs recorded in the MUNIS system (not covered in our sample) were issued for 1,447 units valued at $1.1M, ranging from $700 to $170K. Similarly, these appeared artificially divided to qualify as a small purchase. The cost of the 45 POs totaling $1.5M, could have been subjected to the OAG review as the procurement value exceeded $500K. Therefore, we questioned the cost of these POs aggregating $1.5M with the appearance of artificial division.

Noncompliance with Asset Management SOPs

1. Inconsistencies with DONs, POs and Distribution Plans

Under GDOE SOP#200-015 Section 3.1.1, a distribution plan should be established before any incoming assets/equipment are allocated/delivered to the school/division and end-users.

a. PO No. 20221094-Requisition #20221923- LENOVO 81MB67US/LENOVO NOTEBOOK- $340K

DON states, “to procure technology for student use for 25 public schools.” However, per the Acceptance of Receipt duly signed by the GDOE personnel who received the laptops, 1,050 laptops were only distributed to 5 public schools, exceeding or short of the Distribution Plan. VSA Benavente Middle School was distributed 360 laptops, although the school is not included in the Distribution Plan, while 20 schools did not receive any of the allotted 840 laptops. The Acceptance Receipt reflects that the Distribution Plan was not followed in the distribution process.

b. PO No. 20210476- Requisition No. 20210221 – Lenovo L13 YOGA

We identified inconsistencies between the receiving report and distribution plan for laptops that were delivered to six schools. Per the Distribution Plan, one school was allocated 150 to 210 units, however, actual distribution was either none or a maximum of 450 units.

Weaknesses in Internal Controls

1. Discrepancies in Physical Inventory and MUNIS Inventory Records

Our physical count of laptops in 10 selected GDOE schools found discrepancies between the MUNIS inventory record (as of May 5, 2023). One school had 53 laptops, more than what was recorded on the MUNIS inventory records. All other nine schools had a physical count that was less than what was recorded on the MUNIS inventory records, ranging from 11 to 174 laptops. The discrepancies are indicative of non-reconciliation of physical assets against the recorded transactions and a lack of periodic monitoring of the physical existence of the assets.

Other Matters

During our review, we found some issues which are not within our audit objectives, however, we believe these matters need to be communicated to the GDOE management for remedial action. These matters include GDOE’s inability to retrieve all laptops issued to students and inadequate secured laptop storage. GDOE management needs to address these prevailing issues relative to physical control, adequate storage, and infrastructure to preserve its assets and minimize potential waste in the use of public funds and resources.

Conclusion and Recommendations

We uphold GDOE management’s decisive action, determination, and effort to respond to the needs of a significant Guam student population to provide the best education during the period of the COVID-19 pandemic. The tasks of planning, fund sourcing, procurement and purchasing and distribution to the ultimate end-users is a great responsibility shouldered by the GDOE and other government officials. However, these actions and decisions need to be performed in adherence to Guam Procurement law and regulations and GDOE internal policies and procedures with great consideration of internal controls in executing processes.

As a significant amount of federal funds was used for the purchase of these laptops, GDOE needs to institute corrective measures to prevent more recurrences and ensure efficient use of local and federal resources in order that excess funds be properly allocated to other viable government programs. We made 11 detailed recommendations relative to procurement and internal controls.

2 Comments

Frenchie

03/04/2024 at 12:58 PM

What is amazing, beside the huge issue of corruption, is the fact that these geniuses opted for a Lenovo product. Knowing we have a target on our back regarding cyber security, they decided to go with a company known for its ties with CCP spies agencies, and imbeded back door access. Corruption is one thing, stupidity at a suicidal level is another story. I guess you can’t fix stupid. To think that Josh wants to run on this kind of record is mind blogging

PJ

03/04/2024 at 7:56 PM

Who is the Vendor? Let me guess …Gov/Lt Gov “I’m In!” Treasurer, Toni Sanford. Check out other other Transition Team’s agencies who profited from the Lenovo scam!